[ad_1]

The local online food delivery market is estimated to touch .53 billion by 2023, according to estimates by DataLabs by Inc42.

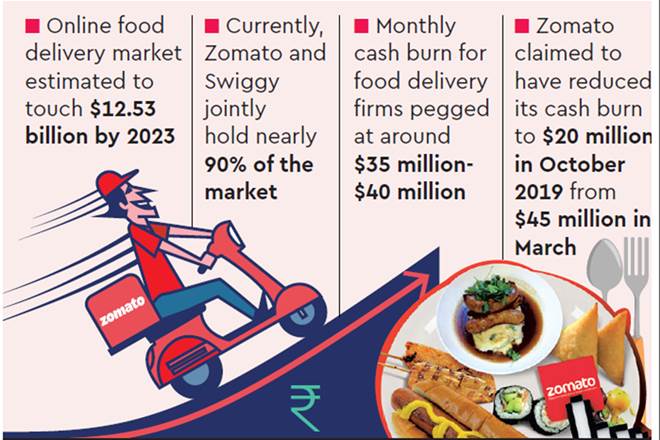

The local online food delivery market is estimated to touch .53 billion by 2023, according to estimates by DataLabs by Inc42.Food delivery player Zomato is closing in on UberEats’ India business, sources familiar with the development told FE, setting the pitch for a bruising fight between the Gurgaon-based firm and Swiggy. The negotiations have entered into the final stages, the sources said. The local online food delivery market is estimated to touch $12.53 billion by 2023, according to estimates by DataLabs by Inc42. If the deal fructifies, Zomato will get the backing of an investor of the stature of Uber and support to fight a competitor.

In turn, Uber secures a good exit from the food delivery vertical which is not top priority in India, Satish Meena, senior analyst at Forrester Research, pointed out. Zomato’s offerings will become more diversified since its platform is skewed towards mid-range to premium restaurants, analysts said.

Nonetheless, fighting off Swiggy will not be that easy for Zomato. “Swiggy dominates the food delivery market and even after Zomato-UberEats deal, it will stay the largest,” said Meena. While Swiggy delivers about 42 million orders per month, Zomato delivers around 36-37 million orders. Currently, Zomato and Swiggy jointly command nearly 90% of the market — while Swiggy leads with a 48% market share, Zomato holds about 42%, according to industry estimates.

The monthly cash burn for Zomato and Swiggy is estimated to be around $35 million-$40 million. Recently, Zomato claimed to have reduced its cash burn to $20 million in October 2019 from $45 million in March. For smaller player like UberEats, the burn is pegged at around $4 million-$5 million per month. UberEats made its India launch in 2017 and operates in over 40 cities. Zomato is present in over 500 cities.

Zomato’s advertising promotional expenses increased to Rs 1,213.61 crore in FY19 from Rs 80 crore in FY18. Swiggy’s expenses on the front rose to Rs 776.2 crore from Rs 129.8 crore. Zomato’s losses increased to Rs 570.52 crore in FY19 from Rs 78.49 crore in FY18. Founder and CEO Deepinder Goyal believes the company will turn profitable by the end of 2020.

Given that Zomato’s other service verticals like events, Gold programme will take time to scale up and generate considerable revenue, reducing cash burn will be a challenge as food delivery is an expensive category, analysts said. Growth in the sector which was primarily driven by discounts in the last 12-18 months is now saturating. Also, food delivery players are facing the wrath of restaurants on charges of arbitrary commissions. “Moreover, Swiggy is becoming more aggressive on the delivery part. Zomato has to spend a lot to capture the market share in delivery,” an analyst said on condition of anonymity. Reportedly, Uber is in talks to invest $100-200 million in fresh capital as part of the sale. The fund infusion will be a critical part of the share-swap deal between the two firms, the Economic Times reported last month.

Zomato has raised $150 million from existing backer Ant Financial. The fundraise, which is part of a larger deal, gives it a pre-money valuation of $3 billion, parent Info Edge said in a stock filing on Friday. The share swap deal is likely to consider the $3 billion valuation, according to media reports.

Earlier last year, Uber in its IPO (initial public offering) filing had said Swiggy and Zomato have significant product advantages as the companies have substantial market-specific knowledge and established relationships with local restaurants. “As a result, such competitors may be able to respond more quickly and effectively than us in such markets to new or changing opportunities,” Uber had said. Uber Technologies posted its largest-ever quarterly loss, a whopping $5.24 billion in the three months ended June 2019. Losses remained elevated at $1.2 billion in Q3 2019.

Get live Stock Prices from BSE and NSE and latest NAV, portfolio of Mutual Funds, calculate your tax by Income Tax Calculator, know market’s Top Gainers, Top Losers & Best Equity Funds. Like us on Facebook and follow us on Twitter.

[ad_2]

Comments are closed.